Beyond the Illusion: The Predatory Reality of Modern Installment Loans

Modern finance is designed to disconnect you from reality. "Buy Now, Pay Later" (BNPL) is a strategic trap engineered to lure shoppers into debt for items with zero long-term value.

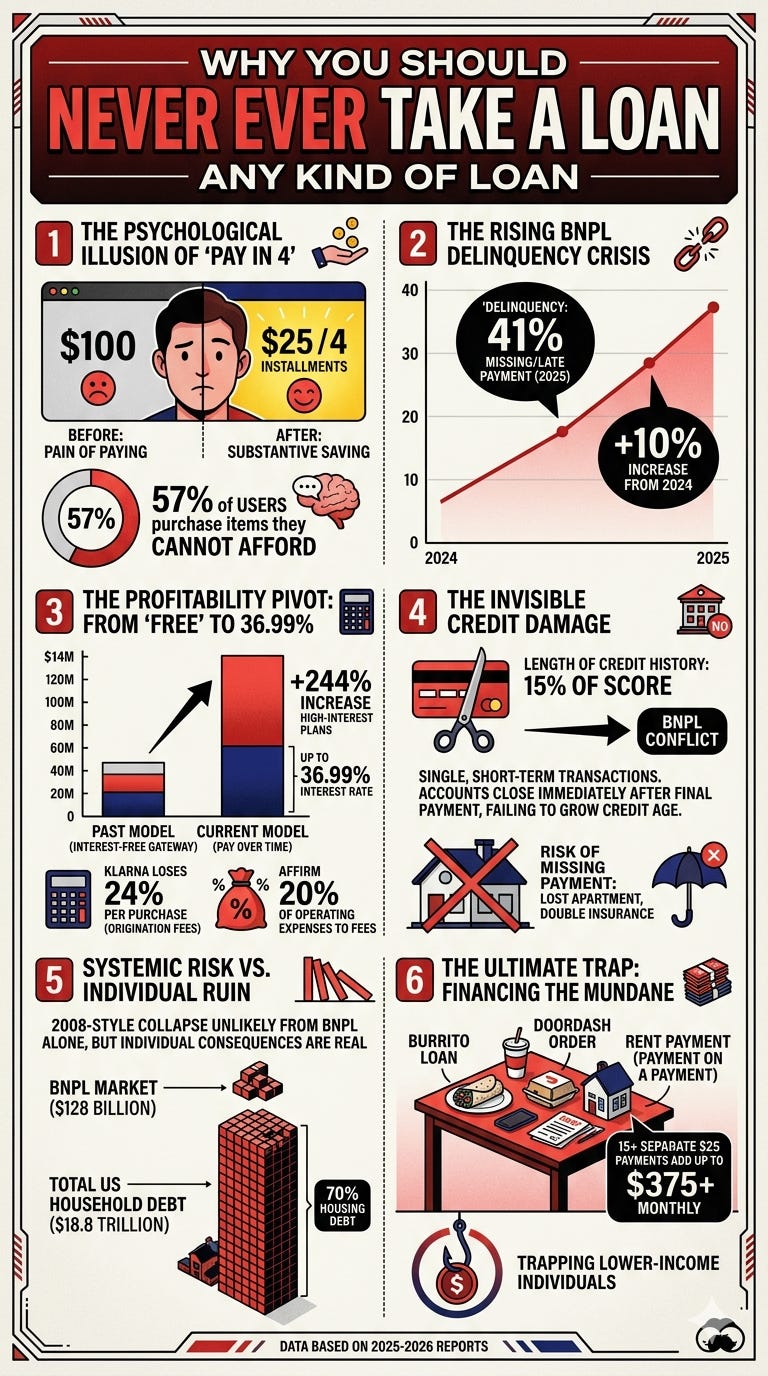

The "Pay in 4" Illusion

BNPL bypasses your brain's natural resistance to spending. By breaking a $100 price into four $25 installments, consumers feel they are "saving" $75. This psychological trick leads 57% of users to buy things they cannot afford.

The Delinquency Crisis

2025 data shows the "solution" is failing. 41% of BNPL loans had late payments—a 10% jump from 2024. Nearly 20% of Americans use these services, with younger generations seeing the highest failure rates.

Predatory Profit Models

BNPL firms are software middlemen, not banks. To reach profitability, they are pivoting to high-interest "Pay Over Time" plans with rates up to 36.99%. This revenue segment grew 244% last year. Klarna loses 24% of each purchase to origination fees, and 20% of Affirm's total operating expenses go to these fees. They must trap users in interest-bearing cycles to survive.

Invisible Credit Damage

15% of a credit score depends on history length. BNPL accounts close immediately after the final payment, failing to build your credit age. Users face the risk of missed payments—which can block apartment rentals or double insurance costs—without the benefit of a rising score.

Systemic vs. Individual Risk

The $128B BNPL market is small compared to the $18.8T U.S. household debt. While a 2008-style collapse is unlikely (as housing debt is 70% of that tower), individual ruin is real. Financing daily needs like burritos or rent creates a "payment on a payment," trapping lower-income individuals in a comple

x web of micro-debt.