Nuclear in a Box: Why Small Modular Reactors Are the Only Real Choice Left for the AI Power Crisis

How Tech Giants Are Forcing a High-Stakes Nuclear Revival to Save the AI Grid from Collapse

The grand plan to swap out our massive, centralized nuclear plants for shiny new Small Modular Reactors (SMRs) is hitting the exact same wall that every overhyped tech revolution faces: reality. Right now, AI-driven data centers are staring down an unprecedented power crunch, creating a frantic scramble between cutting-edge technology, desperate manufacturers, and absolute geopolitical bottlenecks. According to the International Energy Agency 2026 Data Center Energy Report, the collective electricity consumption of global data centers, AI, and cryptocurrency is skyrocketing, climbing from 460 terawatt-hours in 2024 to over 1,000 terawatt-hours. To put that in perspective, that is roughly equal to the entire energy consumption of Japan.

To keep the lights on, hyperscaler capital expenditure for direct AI infrastructure has crossed into the eye-watering territory of 725 billion to 805 billion dollars in 2026. Tech conglomerates are realizing they can no longer just buy energy from the local grid; they have to become primary infrastructure financiers. The baseline model from Goldman Sachs Research’s May 2026 report, "Tracking Trillions: The Assumptions Shaping the Scale of the AI Build-Out," projects annual AI capital expenditure hitting 765 billion dollars this year and accumulating to 7.6 trillion dollars by 2031. Goldman Sachs details that the cost of building next-generation AI data centers has spiked from 10 million dollars per megawatt for traditional cloud infrastructure up to 15 million to 20 million dollars per megawatt due to the extreme cooling and power density requirements of AI chips.

The renewable energy strategy favored by these tech giants—relying on massive wind and solar installations—is fundamentally failing to meet this demand. Wind and solar are inherently intermittent, operating at low capacity factors (typically 25 to 40 percent) compared to baseload power. AI data centers require a continuous, uninterrupted 24/7 power supply at a 99.999 percent uptime reliability rate. Data from Lawrence Berkeley National Laboratory highlights that the structural mismatch between variable renewable generation and flat data center load profiles forces continuous reliance on fossil-fuel backup or grid-stabilizing assets, meaning wind and solar alone lack the energy density and reliability required to sustain hyperscale AI expansion without a stable baseload anchor.

The Baseload Replacement Fallacy and the Coal Irony

This structural gap creates a brutal infrastructure irony. Tech companies are publicly committed to phasing out fossil fuels, and SMR proponents pitch these reactors as the perfect plug-and-play solution to drop directly onto the graves of retired coal plants to hijack their existing grid connections. But because SMR deployment timelines are lagging years behind the immediate power crisis, utility companies are being forced to extend the operational lifespans of those exact coal plants just to keep the AI grid from collapsing. Instead of a clean transition, the delay in advanced nuclear deployment is actively locking in coal and natural gas dependency.

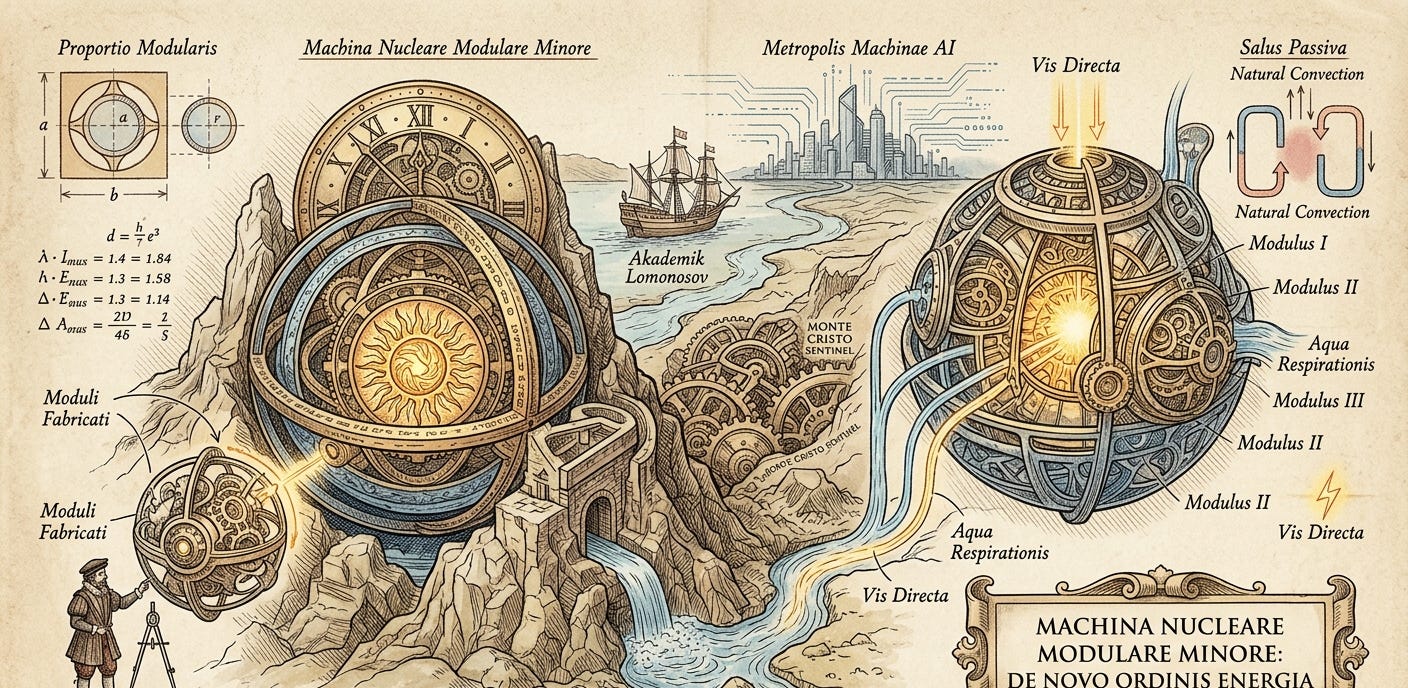

Defining the Small Modular Reactor

For the uninitiated, a Small Modular Reactor is a nuclear fission reactor with a power capacity capping out at 300 megawatts electric per unit. That is about one-third the output of a traditional plant, according to the International Academy of Atomic Energy SMR Standard Definition. The real marketing magic here is the word "modular." The pitch is simple: design them to be factory-built, slap them onto a railcar or a semi-truck, and assemble them on-site. In theory, this transforms nuclear power from a multi-decade civil engineering nightmare into a streamlined industrial product.

Technical Specifications and Architecture

The big technical brag for these reactors is the transition to passive safety systems. Traditional reactors require active pumps and a reliable external electricity supply just to keep from melting down, but SMRs lean on basic physics like gravity and natural convection. If the facility completely loses power, the coolant keeps right on circulating, and heat dissipates through the reactor vessel without a human being lifting a finger, as detailed in the International Atomic Energy Agency 2024 SMR Technology Booklet.

Because they take up a remarkably small footprint, they require significantly less cooling water than legacy gigawatt plants, meaning they can theoretically be deployed inland or in arid environments. This makes them highly appealing for heavy industrial sites and large-scale desalination plants, which currently command a 30 percent slice of the SMR market share according to Coherent Market Insights.

The Global Manufacturing Race

The geopolitical map is currently split between countries actually building hardware and Western corporations signing non-binding agreements. Russia is leading the floating category with its Akademik Lomonosov, which recently completed its first full fuel cycle, while pushing forward with the BREST-OD-300 lead-cooled reactor, slated to reach criticality by 2028 according to the Rosatom Status Report. China is dominating the land-based race with its gas-cooled HTR-PM, which went into commercial operation in December 2023. Their ACP100, known as Linglong One, is undergoing final testing and is scheduled to log commercial operation in the first half of 2026, securing its title as the world's first land-based commercial unit of its kind, per a China National Nuclear Corporation announcement.

Meanwhile, Western nations are attempting to scale up through corporate matchmaking. In the United Kingdom, Rolls-Royce SMR signed a major contract on April 13, 2026, to deliver three units at Wylfa, Wales, backed by up to 599 million pounds of financing from the National Wealth Fund and Great British Nuclear. Over in the United States, NuScale Power, X-energy, and Oklo are the names to watch. Oklo managed to secure a massive 12-gigawatt non-binding power agreement to feed AI data centers. Tech giants are opening their own wallets, too. Amazon led a 500 million dollar funding round for X-energy to chase a target of 5 gigawatts of capacity by 2039, alongside secondary deals with Energy Northwest and Dominion Energy. Google signed its own fleet purchase agreement with Kairos Power for 500 megawatts across multiple reactors, hoping to see the first unit go live by 2030 using molten-salt cooling and ceramic pebble-type fuel.

The Strategic Perspective: Hidden Dimensions

Because SMRs are scattered across the landscape rather than tucked away in a single fortified compound, they come with a completely different security headache. Proponents like to argue that burying them underground makes them tough targets for kinetic military strikes. Critics look at the same picture and see a proliferation nightmare. The Bulletin of the Atomic Scientists points out that shipping fully fueled reactor cores across international borders makes tracking nuclear material a regulatory mess. A decentralized grid simply gives saboteurs a much broader menu of targets.

Then there is the waste paradox and a localized resource bottleneck that the industry prefers not to talk about. SMRs are marketed as clean, but most still create radioactive byproducts. The Proceedings of the National Academy of Sciences indicates that the spent fuel generated per kilowatt-hour can actually be higher than in large-scale reactors because smaller cores are less efficient at utilizing fuel.

Even worse is the water bill. A standard SMR configuration guzzles roughly 15 million gallons of water every single day for cooling. Data from the World Resources Institute reveals that two-thirds of all data center projects built or developed since 2022 are packed into high water-stress zones like southern Arizona, Texas, and the Colorado River Basin. This massive physical footprint has triggered an intense public backlash, turning local community consensus into a multi-billion dollar liability.

According to May 2026 tracking data from Trellis, organized community opposition has locked up 18 billion dollars in United States data center projects and delayed another 46 billion dollars since mid-2024. That is a 64 billion dollar blind spot. There are now at least 188 active local opposition groups operating across 40 states, and 12 states have already introduced moratorium bills to halt new data center permits. In Q1 2026 alone, at least 20 proposed data centers were cancelled due to this backlash, erasing 42 billion dollars of planned capital expenditure before the first concrete pour.

This friction is turning into severe political fallout. In Virginia, the literal heart of global data infrastructure, public anger over climbing electricity bills and dried-up water resources has already cost local politicians their seats in primary elections. In May 2026, a massive public uproar broke out in Utah over a proposed facility in Box Elder County fueled by fears of localized temperature spikes and water depletion near the already dying Great Salt Lake. On the international stage, courts in Chile completely halted a major Google data center project after local communities discovered it would pull more than 7 billion liters of water annually from endangered regional aquifers.

The Competitive Threat and the Paradox of Low Adoption

The window for SMRs to dominate the market is closing fast. While nuclear projects wade through mud, enhanced geothermal energy and long-duration battery storage are getting cheaper by the minute. Private fusion companies are sucking up billions in venture capital, aiming for net-gain milestones that could render fission-based SMRs obsolete before they even finish building the factories, according to the Bloomberg New Energy Finance Outlook. Because SMR timelines realistically stretch out between five and ten years, hyperscalers are forced to fund the resurrection of ancient, gigawatt-scale civilian reactors just to buy time. Microsoft proved this by signing a landmark 16 billion dollar, 20-year Power Purchase Agreement with Constellation Energy to wake up the 835-megawatt Crane Clean Energy Center at Three Mile Island Unit One by 2028.

Actual SMR adoption remains paralyzed by three fundamental hurdles. First, the first-of-a-kind financial trap makes initial units obscenely expensive, occasionally hitting 15,000 dollars per kilowatt in early Western projects according to World Nuclear News. Investors are naturally terrified of funding a prototype until someone else proves mass production works.

Second, there is the legendary regulatory lag. Nuclear regulators are fundamentally built to inspect slow, bespoke construction projects. While tech companies have signed agreements for over 45 gigawatts of power, licensing timelines drag out for a decade, completely missing the agile two-year build cycle of an AI data center. The United States tried to patch this by passing the ADVANCE Act and pushing the Nuclear Regulatory Commission to finalize its Part 53 licensing framework, attempting to compress reviews into an 18-to-24 month window for pre-approved designs.

However, the Western regulatory landscape is completely fractured. While Europe has attempted a similar shortcut with the European Industrial Alliance on SMRs to harmonize cross-border red tape, the continent remains a bureaucratic black hole. Germany has entirely abandoned nuclear energy, France is doubling down on its national champion EDF, and cross-border regulatory harmonization across the EU remains a legal fantasy. An investor wanting to deploy an SMR fleet across multiple European jurisdictions faces a decade of isolated legal battles rather than a unified approval process.

Third, the High-Assay Low-Enriched Uranium (HALEU) supply chain is broken. Russia is the only game in town for commercial HALEU fuel. The United States Department of Energy poured 2.7 billion dollars into domestic enrichment to fix this, but a fully operational, independent supply chain is still years away.

Conclusion

The Small Modular Reactor revolution is a strategic necessity forced by an aggressive AI infrastructure explosion. But until Western nations can secure their own fuel lines, resolve local resource conflicts, and force Cold War-era regulators to move at digital speed, these "reactors in a box" will remain highly expensive science experiments, while China and Russia continue to run away with the actual market advantage.