THE SUBPRIME EXTRACTION ENGINE: How Predatory Lenders Bleed Low-Income Consumers, Discard the Defaults, and Import New Targets

Inside the predatory system that bleeds low-income Americans dry, exploits their defaults, and resets the loop.

Welcome to the modern economic grid, where the lower-income population does not actually possess wealth; they merely rent it for brief intervals before passing it upward.

In mainstream economic theory, a consumer is a rational actor who builds credit, buys assets, and constructs a life. In reality, a massive chunk of the population exists purely as infrastructure. This is the Human Conduit Theory.

As I theorize here, a Human Conduit is a low-income consumer who functions strictly as a financial pipeline. Rather than accumulating assets or building long-term generational wealth, their economic role is restricted to absorbing capital—via subprime credit markets, predatory loans, or state safety net assistance—and immediately flushing it directly into corporate balance sheets. They are human plumbing, built to transport cash from point A to point B, until the friction of high interest and systemic debt breaks the pipe entirely. The empirical realities of the modern economy heavily substantiate this framework, with hard data backing up every stage of the loop.

The Post-Bank Extraction Phase

Let us examine what happens when a citizen’s credit score hits the floor—specifically, a pristine 341. Mainstream commercial banks will not even let you breathe their filtered air, let alone borrow money. But do not worry, the free market hates a vacuum. Right past the gated doors of traditional banking lies the highly lucrative Post-Bank market.

The institutions running this sector do not look at your 341 credit score with pity; they look at it with dollar signs. They do not care that you cannot afford the asset. They do math, adjust the dials, and deliberately design a loop meant to extract maximum revenue before the inevitable collapse.

According to the Consumer Financial Protection Bureau (CFPB), standard payday lenders charge a casual $15 fee for every $100 borrowed on a two-week loan. In standard language, that is an Annual Percentage Rate (APR) of roughly 400%. The business model is literally built on failure, with CFPB data showing that over 80% of these loans must be rolled over or renewed within 14 days because the borrower cannot actually pay it back.

If you do not have a steady paycheck to leverage, they will happily take your physical car title instead. CFPB tracking reveals that 83% of auto title loan users and 73% of pawn loan users are still stuck owing money six months after taking out the loan.

Turn over to the subprime auto loan market, and the picture becomes even clearer. Data from Fitch Ratings shows that the 60-plus-day delinquency rate for subprime auto asset-backed securities hovers near 6.74%. While subprime borrowers make up a fraction of total automotive accounts, they carry nearly two-thirds of all vehicle defaults nationwide.

The dealership knows you will default. They want you to. They take your $2,000 down payment, let you make one or two high-interest payments, repossess the car using hidden GPS trackers you paid for, and put it right back on the lot for the next pipeline worker.

Systemic Disposal and the Cash Economy

So what happens when a conduit is completely bled dry? When the wages can no longer be garnished because the individual is forced to leave the traditional grid entirely? The system does not attempt to repair the pipe. It activates a disposal protocol.

Under Internal Revenue Code (IRC) Section 166, the corporation simply writes off the defaulted loan as a charge-off bad debt expense, lowering its own corporate tax burden. They take the tax break, keep the asset, and walk away.

The individual is cast out into the underground cash economy. According to data from the Federal Reserve Board, a staggering 23% of American adults with a family income under $25,000 are completely unbanked, operating primarily or entirely within a cash-only framework. The FDIC corroborates this baseline economic disconnect, confirming that 4.2% of all U.S. households operate entirely outside the traditional banking ecosystem, with 66.2% of them relying purely on physical cash to survive, while another 14.2% are trapped in the underbanked twilight zone—paying predatory fees just to cash a paycheck or purchase a basic money order.

At this exact moment, the corporate sector socializes the cost of their collateral damage. The long-term survival of the broken domestic conduit is shifted entirely onto public safety nets—SNAP, Medicaid, and welfare. The state picks up the bill to keep the person alive, while that same government assistance is immediately spent right back at corporate grocery chains and retailers.

The Replacement Metric

Here is the final twist in the architecture. The system cannot function without a high volume of active, flowing pipelines. If 22% to 23% of the low-income population becomes financially broken and drops out of the traditional credit loop, corporate revenues face a massive vacuum.

The solution is not to rehabilitate the domestic underclass. The solution is to import fresh, highly efficient conduits who are eager to plug into the extraction machine.

The vacuum is filled through highly regulated, corporate-friendly immigration pipelines. Data from U.S. Citizenship and Immigration Services (USCIS) confirms a strict statutory annual cap of 65,000 new H-1B visas, plus an additional 20,000 advanced degree exemptions, guaranteeing a fresh baseline corporate intake of 85,000 highly controlled workers every single year.

The demand for these slots is fiercely competitive, with USCIS tracking historic registration volumes peaking at 780,884 applications in a single cycle, and stabilizing at 470,342 in subsequent years.

This vast pool of legal and illegal labor serves an essential macroeconomic purpose. They enter the system with an urgent need for baseline consumption, used vehicles, housing, and credit. They have no financial scars yet. They are clean, unblemished pipelines ready to take the place of the discarded domestic workforce, resetting the subprime extraction loop from the exact beginning.

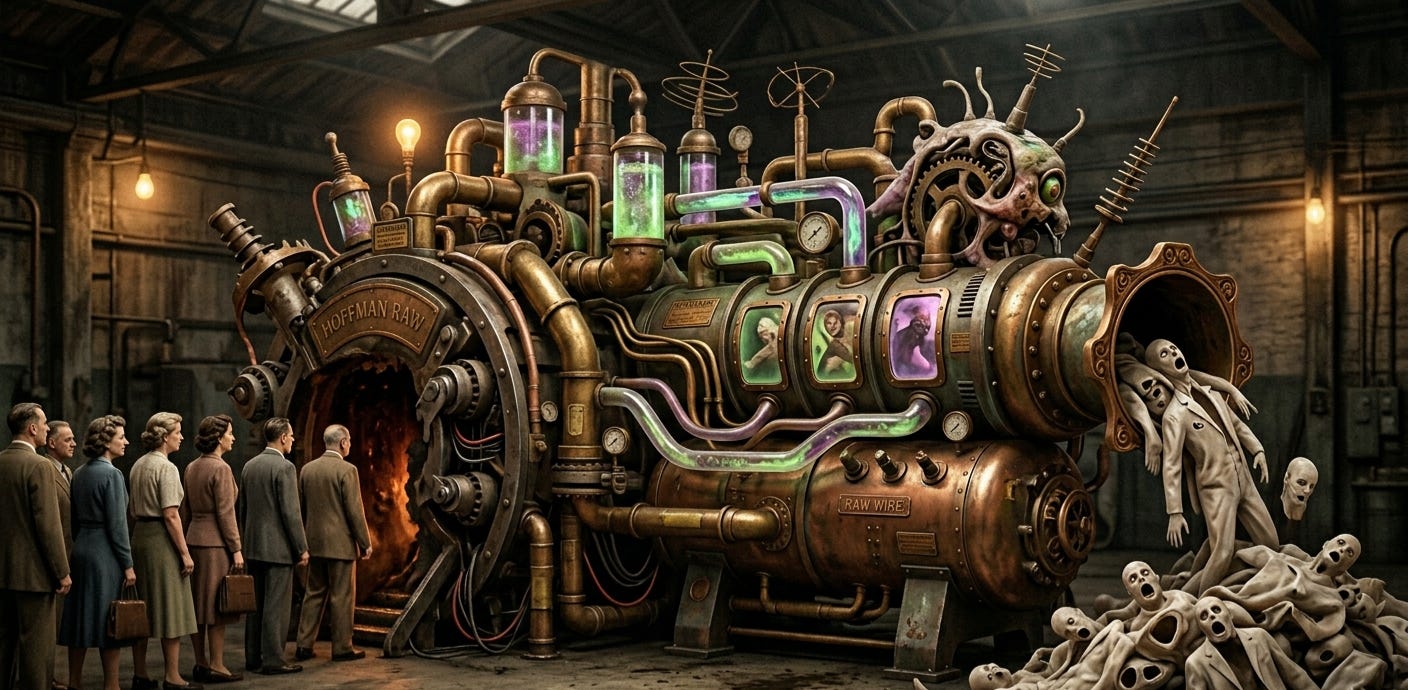

The Hoffman Raw Wire Verdict

The machine does not care about a 341 credit score because the machine does not need the consumer to succeed. It needs them to flow. Under the Human Conduit Theory I have formulated here, the low-income consumer is not viewed by the post-bank market as a wealth-building actor, but as disposable financial infrastructure. When the individual stops flowing, the system writes them off for a corporate tax deduction under IRC Section 166, shifts their long-term survival costs to the taxpayer, and utilizes regulated immigration intakes to install a fresh, unblemished replacement pipeline—resetting the predatory subprime extraction loop from the absolute beginning. Real-world data from the CFPB, the Federal Reserve, the FDIC, and USCIS fully back this metric, exposing an economic grid that relies on deliberate, structural replacement to maintain upper-tier corporate revenues.